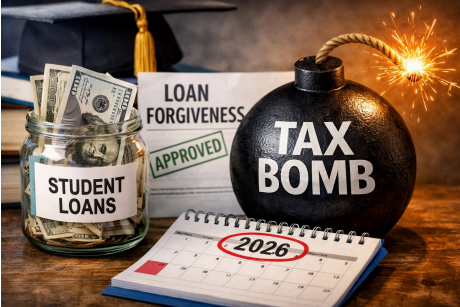

Imagine you have been paying on your loans for two decades. You have done the work and stayed on your plan. Finally, you see that beautiful zero on your account. You celebrate. You might even go out for a nice dinner. Then, tax season rolls around. The IRS typically views canceled debt as taxable income. If you had fifty thousand dollars in loans forgiven, the IRS looks at that exactly like you just earned an extra fifty thousand dollars in salary. If you are already in a mid-level tax bracket, that extra "income" could easily push you into the highest bracket possible. Suddenly, you do not owe the bank anymore, but you owe the IRS fifteen or twenty thousand dollars. Unlike your student loans, the IRS is not usually interested in a twenty-year payment plan with low interest

Read More